Global News

ANA vs JAL: Intensifying Route Rivalries

6 min read

By Matthew H.

ANA and JAL: Strong Demand and Intensifying Route Rivalries

Tokyo, [February 17] — The airline industry is steadily rebounding from the impact of COVID-19, and Japan’s leading carriers, ANA Holdings and Japan Airlines (JAL), are at the forefront of this recovery. Both carriers have demonstrated impressive revenue growth in the third quarter of the fiscal year ending March 2025, driven largely by a resurgence in passenger travel across international and domestic markets. This analysis explores their performance, focusing on passenger travel while briefly covering cargo and low-cost carrier (LCC) segments. Special attention is given to the heated competition on popular routes—such as the Hong Kong–Tokyo corridor, where ANA (and its partner Peach Aviation on the HK–Osaka leg) and JAL are now competing with Cathay’s HK Express.

──────────────────────────────

1. Recovery and Growth

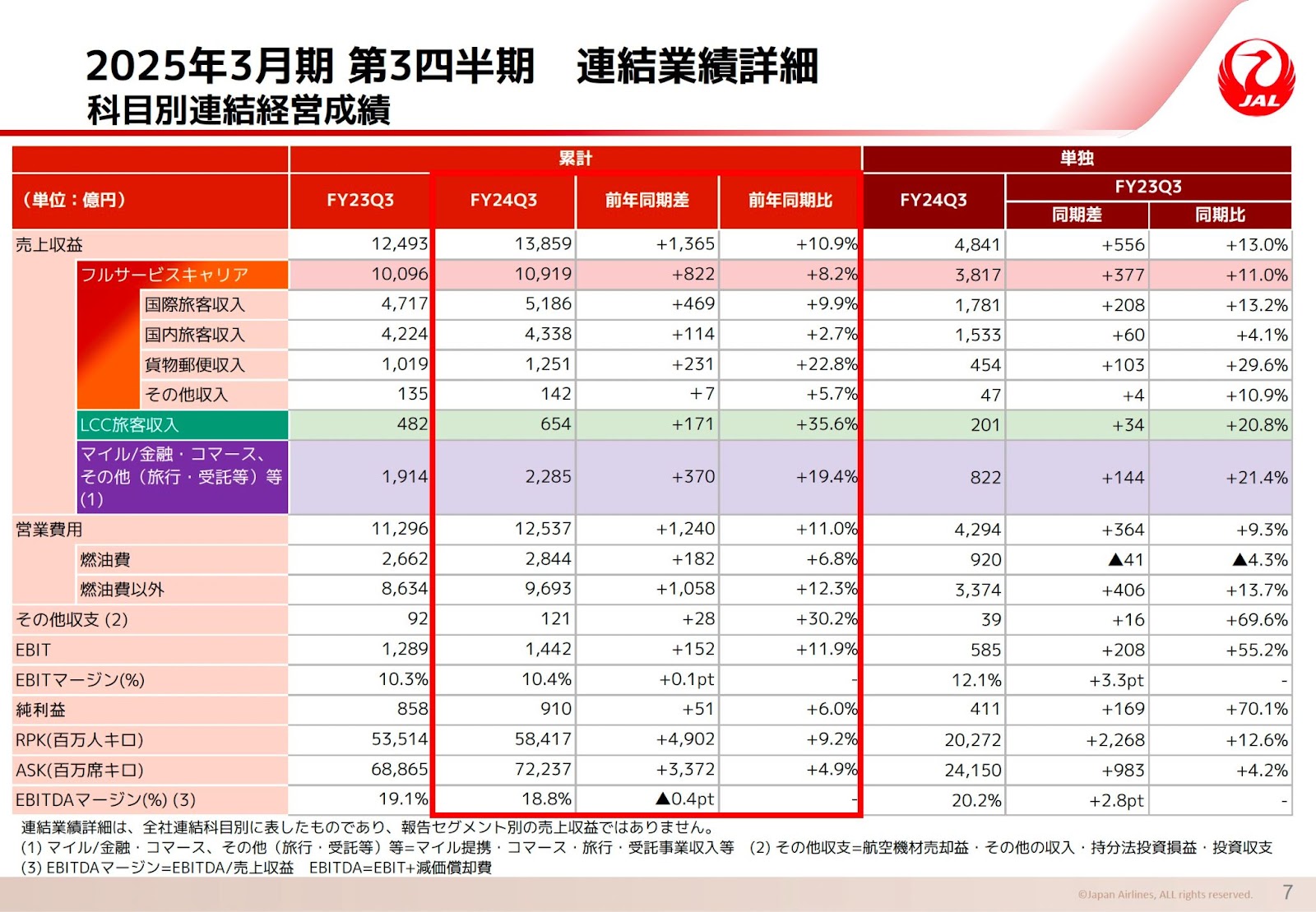

The airline industry has emerged from the challenges of COVID-19 and is now entering a new growth phase. In the Q3 period of the fiscal year ending March 2025 (April–December 2024), both ANA Holdings and Japan Airlines (JAL) delivered encouraging results. ANA’s revenue reached ¥1.7027 trillion—up 10.3% year-on-year—while JAL posted ¥1.3859 trillion, an increase of 10.9%. A recovery in international travel demand and robust domestic passenger travel largely drives this two-digit growth.

──────────────────────────────

2. Passenger Travel: The Heart of the Recovery

Passenger travel remains the core strength behind both companies’ financial performances.

International Routes:

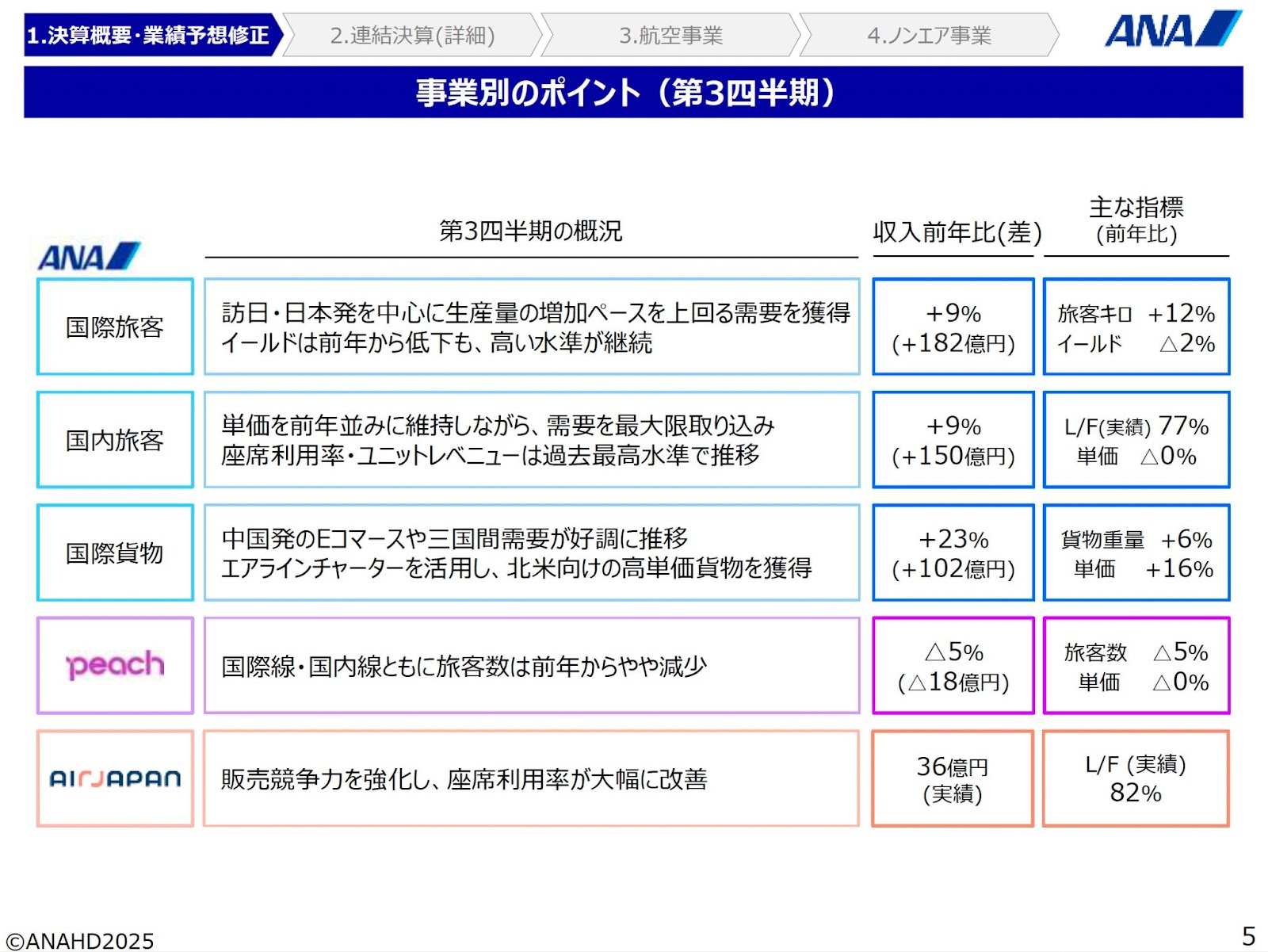

For international operations, ANA recorded revenue of ¥800 billion (up 9.0% YoY) and JAL reported ¥518.6 billion (up 9.9% YoY). ANA’s strong performance on transatlantic routes, particularly to Europe and North America—with high yields from First and Business Class cabins—has been a major contributor. Meanwhile, JAL has seen notable recovery on Asian routes, benefiting from increased inbound tourism from China and Southeast Asia.

Domestic Routes:

Domestically, ANA outperformed with ¥701 billion in revenue (up 9.0% YoY) compared to JAL’s ¥433.8 billion (up 2.7% YoY). ANA’s strategic focus on boosting regional travel and tapping into local tourism demand has paid off, positioning it ahead in the domestic market. Although JAL also enjoyed a boost from leisure travel recovery, its smaller network size is reflected in the revenue gap when compared with ANA.

──────────────────────────────

3. Cargo and LCC Segments: In Brief Yet Crucial

Cargo & Mail Business:

Both airlines posted strong gains in their cargo segments, with ANA achieving ¥218 billion (up 23.0% YoY) and JAL reaching ¥125.1 billion (up 22.8% YoY). The sustained demand for international cargo, especially driven by robust e-commerce shipments from China, has been a bright spot.

LCC Operations:

In the low-cost carrier arena, competition is heating up. ANA, operating Peach Aviation and AirJapan, reported LCC revenues of ¥151.0 billion (an increase of ¥11.6 billion YoY) while JAL’s ZIPAIR delivered ¥65.4 billion (up ¥17.1 billion YoY). Notably, on the busy Hong Kong–Tokyo route—which has seen a strong post-pandemic rebound—ANA and JAL are now directly contesting with Cathay Pacific’s oneworld-affiliated LCC, HK Express. Similarly, on the Hong Kong–Osaka route, Peach Aviation has stepped up its game in a bid to capture a larger slice of these high-demand markets.

──────────────────────────────

4. The Weight of Costs: Fuel, Labor, and Maintenance

While top-line growth is evident, rising costs are putting pressure on profitability. Key cost drivers include:

• Fuel Costs:

ANA’s fuel expense climbed to ¥309.8 billion (up ¥19.6 billion YoY) and JAL’s to ¥284.4 billion (up ¥18.2 billion YoY). The volatility in fuel prices coupled with a depreciating yen continues to pose significant challenges.

• Personnel Spending:

Increasing labour costs have also impacted margins, with ANA spending ¥172.0 billion (up ¥21.8 billion YoY) and JAL ¥267.5 billion (up ¥23.8 billion YoY). The rise in overseas pay packages due to currency fluctuations has contributed notably.

• Equipment and Maintenance Expenses:

ANA’s aircraft acquisition and leasing costs reached ¥113.9 billion (up ¥1.6 billion YoY), while JAL registered ¥91.5 billion (up ¥500 million YoY). Additionally, maintenance costs surged to ¥176.9 billion for ANA (up ¥54.8 billion YoY) and ¥109.4 billion for JAL (up ¥16.3 billion YoY). ANA’s larger international network and growing cargo fleet have necessitated higher maintenance outlays than JAL.

──────────────────────────────

5. Divergent Strategies and Future Outlook

Both carriers are adapting their strategies to the evolving market, each with its own emphasis:

ANA’s Strategy:

Leveraging a recovering international demand, ANA is expanding its North American and European routes while optimizing cabin configurations to capture higher-yield business and premium-economy travellers. Its aggressive approach to integrating new aircraft types and boosting cargo capacity positions the company to benefit from both passenger and freight market dynamics. In the LCC segment, brands like Peach Aviation and AirJapan are set to strengthen ANA’s competitive offerings in key Asian markets.

JAL’s Focus:

JAL is honing in on improved profitability through rigorous cost control, channelling investments into high-demand routes, and enhancing the efficiency of its operations. Its focused expansion of ZIPAIR in long-haul low-cost travel—targeting markets in North America and Asia—highlights a commitment to agile market responses amid fierce competition. JAL also maximizes the cargo space from its passenger planes to drive incremental revenue in the freight domain.

Competitive Example:

A particularly illustrative case is the competition on the Hong Kong–Tokyo route. Here, both ANA (supported by Peach Aviation’s operations on the Hong Kong–Osaka leg) and JAL, members of the oneworld alliance, are locked in a competitive battle against Cathay’s LCC, HK Express. This route has experienced unprecedented demand post-pandemic, making it a critical theatre for airlines as they strive to capture international leisure and business travellers.

──────────────────────────────

Conclusion

In summary, the third-quarter performance for ANA and JAL in the fiscal year ending March 2025 evidences a strong recovery driven primarily by passenger demand across international and domestic segments. Although both carriers face rising costs—spanning fuel, labour, and maintenance—their strategic initiatives remain robust in the face of evolving market challenges. ANA’s expansive network and premium service offerings complement JAL’s focused cost discipline and efficient route investments. The rivalry on key routes such as the bustling Hong Kong–Tokyo corridor underscores the competitive dynamics in a post-pandemic landscape, promising both challenges and opportunities for these leading Japanese airlines.

Pick Up!

• Q3 fiscal growth: ANA up 10.3%, JAL up 10.9% YoY.

• International and domestic passenger segments drive revenue recovery.

• Rising costs (fuel, labour, maintenance) continue to pressure margins.

• Intense competition on Hong Kong–Tokyo and HK–Osaka routes: JAL vs. Cathay/HK Express, with ANA/Peach also in pursuit

• Strong strategic emphasis on expanding premium and LCC offerings in key markets.

──────────────────────────────

Source:

ANAホールディングス株式会社 2025年3月期 第3四半期決算